Budget officials: low interest rates serve state well at bond sale

It looks like we timed that right.

When Minnesota sells general obligation bonds, it’s best for its budget to do so when interest rates are low. That way, the state will hold down its debt and make more money available to the General Fund over time.

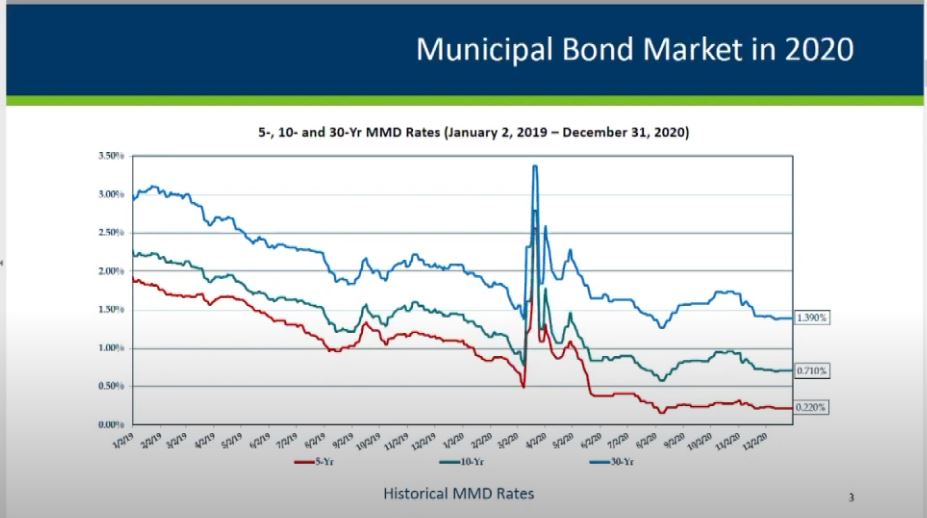

Last March was a bad time for the bond market, with interest rates spiking, then a three-week freeze on sales as the COVID-19 pandemic swept the country. But federal economic stimulus actions soon helped stabilize the market and interest rates descended to record-low levels. Rates, particularly, experienced an August dip — right when Minnesota sold its general obligation bonds to fund infrastructure projects.

“We didn’t look to time the market, but we were certainly successful.”

That’s what Jennifer Hassemer told the House Capital Investment Committee Thursday. She’s Minnesota Management and Budget’s assistant commissioner for debt management. The upshot of her presentation was that the state is comfortably within the range of its capital investment guidelines, and that, as Hassemer said, “You could have a bonding bill of up to $3.23 billion without worries about debt capacity.”

Graphic courtesy Minnesota Management and Budget

Graphic courtesy Minnesota Management and BudgetHassemer made clear that that was in no way a recommendation, just what the state budget is capable of bearing.

In August, Minnesota sold seven series of general obligation bonds, gaining $502.9 million for new or ongoing projects. Interest rates ranged from $1.256% to 1.596%.

The state also refinanced $695.7 million in outstanding bonds, achieving a savings to the state’s General Fund of $47.5 million and, for its trunk highway fund, $57.5 million.

Minnesota Management and Budget’s debt capacity report emphasized three key capital investment guidelines:

- total tax-supported principal outstanding shall be 3.25% or less of total state personal income. It’s currently at 2.27%;

- the total amount of tax-supported principal for state general obligations, state moral obligations (the Housing Finance Agency and Office of Higher Education), equipment capital leases and real estate capital leases shall not exceed 6% of total state personal income. Currently, it’s 3.93%; and

- at least 40% of state general obligation bonds are to mature within five years (that number is 42.3% right now) and 70% within 10 years (currently 75%).

Hassemer added that Minnesota maintains a moderate debt burden compared to other states: “We’ve ranked around the middle of the pack for several years.”

Rep. Jordan Rasmusson (R-Fergus Falls) asked about the state’s current bond rating.

“The state is rated AAA by two bond rating agencies (Fitch and Standard & Poor’s) and one notch below by Moody’s,” Hassemer said. “Generally, they see Minnesota as having the tools to manage through a recession.”

Rep. Nels Pierson (R-Rochester) asked, “What’s keeping Moody’s from giving us a Triple-A rating?”

“Excellent question,” Hassemer said. “They are still taking the long-term view backward around actions that led to government shutdowns. That’s one of the biggest factors holding them back at this time.”

“This seems to me to be an opportunity to build on some of these projects, what with rates low,” said Rep. Leon Lillie (DFL-North St. Paul).

This August’s bond sale will finance projects passed in the 2020 capital investment law.

Related Articles

Search Session Daily

Advanced Search OptionsPriority Dailies

Speaker Emerita Melissa Hortman, husband killed in attack

By HPIS Staff House Speaker Emerita Melissa Hortman (DFL-Brooklyn Park) and her husband, Mark, were fatally shot in their home early Saturday morning.

Gov. Tim Walz announced the news dur...

House Speaker Emerita Melissa Hortman (DFL-Brooklyn Park) and her husband, Mark, were fatally shot in their home early Saturday morning.

Gov. Tim Walz announced the news dur...

Lawmakers deliver budget bills to governor's desk in one-day special session

By Mike Cook About that talk of needing all 21 hours left in a legislative day to complete a special session?

House members were more than up to the challenge Monday. Beginning at 10 a.m...

About that talk of needing all 21 hours left in a legislative day to complete a special session?

House members were more than up to the challenge Monday. Beginning at 10 a.m...