Storm warning: Experts say plan now for state infrastructure damage — or pay more later

Being tops in touchdowns is great if you’re a football team. But not if you’re talking tornadoes.

Minnesota led the nation in tornado touchdowns in 2010 with 144. That was 100 more than the state’s annual average, but 2010 was not an outlier: Storms have gotten worse this century, putting the state among the national leaders in number of catastrophes and associated insurance costs. Hence, homeowner insurance premiums have been getting a lot more expensive in Minnesota.

Those in the fields of meteorology and climatology concur that climate change is the culprit. What it means for the state’s infrastructure – and what can be done to mitigate its effects -- was the focus of Tuesday’s meeting of the House Capital Investment Committee.

The upshot of some compelling testimony from multiple testifiers was that, as the number of catastrophes climbs, things are getting more dangerous, disruptive and expensive. There are many suggestions for limiting damage from floods and storms, the recommendations emphasizing that investments in resilient infrastructure now will save a lot of money later.

The trends identified by testifiers gave the impression that more destruction is probably on the way. On Friday, a joint hearing of the capital investment and climate and energy committees heard about an increase in major rain events in the state. Tuesday’s meeting gave a taste of the financial impact of more frequent and violent storms.

Mark Kulda, vice president of public affairs for the Insurance Federation of Minnesota, laid out some attention-getting numbers.

“Everything changed in 1998,” he said.

That’s when three tornadoes struck one March night, five more on a May day, and “The Southern Great Lakes Derecho” (a major wind storm) hit. They combined to produce $900 million in damage. The year’s total insured losses in Minnesota came to $1.5 billion: more than the sum of losses from the previous 40 years.

But that was just the beginning of the severe storm trend, with flooding also increasing around the state.

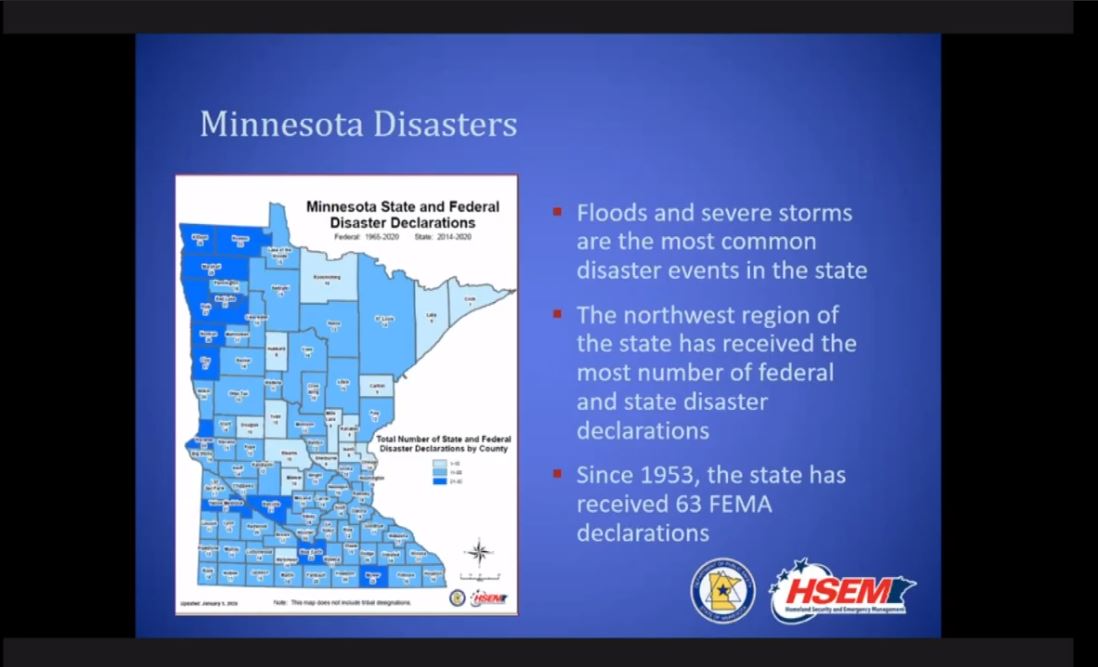

“Disasters have happened in every county in the state,” said Kevin Reed, deputy director of the Minnesota Division of Homeland Security and Emergency Management, “with flooding being the No. 1 disaster that we have.”

In a 2020 assessment by the National Centers for Environmental Information, Minnesota now has the second-most extreme weather in the U.S., behind only California. That’s one factor in why Minnesota’s average homeowner insurance premium went up 366% between 1998 and 2015: It was $368 in 1998, $1,348 in 2015. While the national average has similarly skyrocketed, Minnesota ranked 35th in the nation in cost of insurance premiums in 1998, but is 14th in the latest study.

“Those 100-year floods are happening more frequently,” Reed said. “This will cut into state resources. But it’s been shown that one dollar in mitigation will save you $6 in disaster relief funds.”

What kind of mitigation?

Northfield has moved to limit the kind of floods it experienced four times last decade with “smart” sewer systems that monitor and alter flow, more and larger storm water ponds and infiltration basins, and changing to more permeable pavement. Duluth is rethinking the city’s infrastructure near Lake Superior, choosing not to rebuild some that was damaged in a storm and relocating some out of harm’s way.

And Mankato City Manager Susan Arntz spoke of the city redesigning a riverbank where the Minnesota River is 60 feet wider than it was 12 years ago, in the process shoring up a well that provides 35% of the city’s drinking water.

Reed encouraged every county develop its own mitigation plan, then work through his office to secure federal funding for projects.

“The newest tool is BRIC,” he said. “That’s a program called Building Resilient Infrastructure and Communities. It’s a FEMA (Federal Emergency Management Agency) grant program that covers 75% of the cost. But that required 25% is a challenge for many outstate communities. … But we have a proposal, and we’re recruiting cities to participate.”

Related Articles

Search Session Daily

Advanced Search OptionsPriority Dailies

Speaker Emerita Melissa Hortman, husband killed in attack

By HPIS Staff House Speaker Emerita Melissa Hortman (DFL-Brooklyn Park) and her husband, Mark, were fatally shot in their home early Saturday morning.

Gov. Tim Walz announced the news dur...

House Speaker Emerita Melissa Hortman (DFL-Brooklyn Park) and her husband, Mark, were fatally shot in their home early Saturday morning.

Gov. Tim Walz announced the news dur...

Lawmakers deliver budget bills to governor's desk in one-day special session

By Mike Cook About that talk of needing all 21 hours left in a legislative day to complete a special session?

House members were more than up to the challenge Monday. Beginning at 10 a.m...

About that talk of needing all 21 hours left in a legislative day to complete a special session?

House members were more than up to the challenge Monday. Beginning at 10 a.m...